{kind=link}

By Thomas Piketty

Jun 15, 2021

Last weekend, the G7 ministers announced their intention to apply a minimum tax rate of 15% on the offshore profits of multinationals. Let us be clear: if we leave it at that, it is nothing more and nothing less than the formalisation of a real licence to defraud for the most powerful players. For small and medium-sized enterprises as well as for the working and middle classes, it is impossible to create a subsidiary to relocate its profits or income to a tax haven. For all these taxpayers, there is no choice but to pay ordinary tax. However, if we add up taxes on income and profits and social security contributions, both employees and the small and medium-sized self-employed find themselves paying rates in all the G7 countries well above 15%: at least 20-30%, and often 40-50%, or even more.

The G7 announcement is all the more inappropriate because the proPublica website has just published a vast survey confirming what the researchers had already shown: American billionaires pay almost no income tax compared to the extent of their enrichment and what the rest of the population pays. In practice, the corporate tax is often the final tax paid by the richest (when they pay it). Profits accumulate in companies or ad hoc structures (trusts, holding companies, etc.), which finance most of the lifestyle of the people in question (private jets, bank cards, etc.), almost without any control. . By legalising the fact that multinationals will be able to continue to locate their profits in tax havens at leisure, with a tax rate of 15% as the only tax, the G7 is formalising entry into a world where oligarchs pay structurally less tax than the rest of the population.

How can we break this deadlock? Firstly, by setting a minimum rate higher than 15%, which each country can do right now. As the European Tax Observatory has shown, France could apply a minimum rate of 25% to multinationals, which would bring it 26 billion euros per year, equivalent to almost 10% of health spending. With a rate of 15%, only slightly higher than the rate applied in Ireland (12.5%), which makes the measure harmless, the revenue would be barely 4 billion. Part of the 26 billion could be used to improve the financing of the hospitals, schools and the energy transition ; another part to lighten the tax burden on the self-employed and less prosperous employees. What is certain is that it is illusory to expect European unanimity on such a decision. Only unilateral action, ideally with the support of a few countries, can unblock the situation. Ireland or Luxembourg will undoubtedly lodge a complaint with the European Court of Justice, arguing that the principles of absolute free movement of capital (without any fiscal, social or environmental compensation) defined 30 years ago do not provide for such action. It is difficult to say how the ECJ will decide, but if necessary these rules will have to be denounced and rewritten.

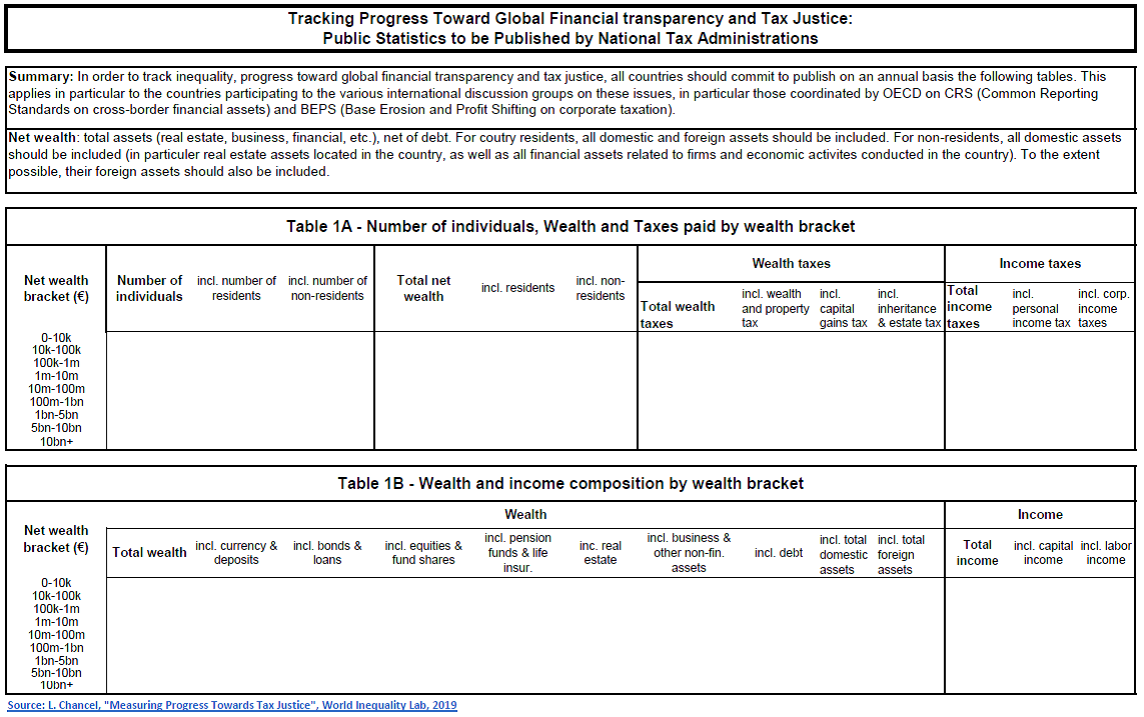

Furthermore, it is urgent to remember that the tax on corporate profits cannot be the final tax for shareholders or managers of companies. It must once again become what it should never have ceased to be, namely an advance payment within the framework of an integrated tax system with progressive income tax at the individual level. The G7 discussions must be explicitly framed within this framework. In theory, rich countries are believed to have implemented systems for the automatic transmission of international banking information on cross-border holdings and individual financial income in recent years. Why, then, do they not publish reliable indicators to measure progress? Specifically, the G7 countries should publish detailed information each year showing the taxes paid by people belonging to very high income and wealth groups (fortunes between 1 and 10 million EUROS, between 10 and 100 million EUROS, between 100 million EUROS and 1 billion EUROS, and so on). Judging by the ProPublica survey, one would probably realize that the wealthiest do not pay much, given the possibilities of downward manipulation of their individual tax income, and that only a progressive wealth tax would make it possible to tax them significantly and in relation to their wealth. . In any case, rather than waiting for the next revelations, all governments should immediately make public the amount of taxes paid by their billionaires and millionaires, especially in France.

{kind=link}

Last but not least, this discussion must finally be opened up to the countries of the South. The mechanism envisaged by the G7, according to which each country is responsible for charging a minimum tax to its own multinationals, is only acceptable if it is an advance payment within a broader system of revenue distribution. The G7 raises the possibility that part of the profits above a certain break-even point (more than 10% per year of the capital invested) will be distributed according to sales in the different countries. But this system will only cover tiny sums and will essentially be reduced to redistribution between the countries of the North. If the latter really want to take up the Chinese challenge, improve their degraded image and above all give the South a chance to develop and build viable states, it is urgent that poor countries have a significant share of the revenues of the multinationals and billionaires of the planet.

Published at www.lemonde.fr